Rust

brokerx — Exchange Gateway

Maintains a persistent WebSocket connection to Deribit.

Normalises the full instrument universe — options, futures,

perpetuals — and publishes order book snapshots, trades, and

user events onto the Redis bus. Handles reconnection with

exponential backoff.

Rust

quantx — Analytics Engine

Calibrates SVI (Stochastic Volatility Inspired) volatility

surfaces every 5 seconds across all active expirations.

Produces parametrised skew metrics — ATM implied volatility,

risk reversal, butterfly spread — and publishes them for

downstream consumption.

Rust

riskofficerx — Risk & Pricing

Computes live portfolio Greeks — delta, gamma, vega, theta —

adjusted for volatility skew. Tracks net exposure across all

positions, enforces risk limits, and exposes a REST pricing

API. Integrates quanto adjustment for USD P&L on

ETH-denominated options.

Rust

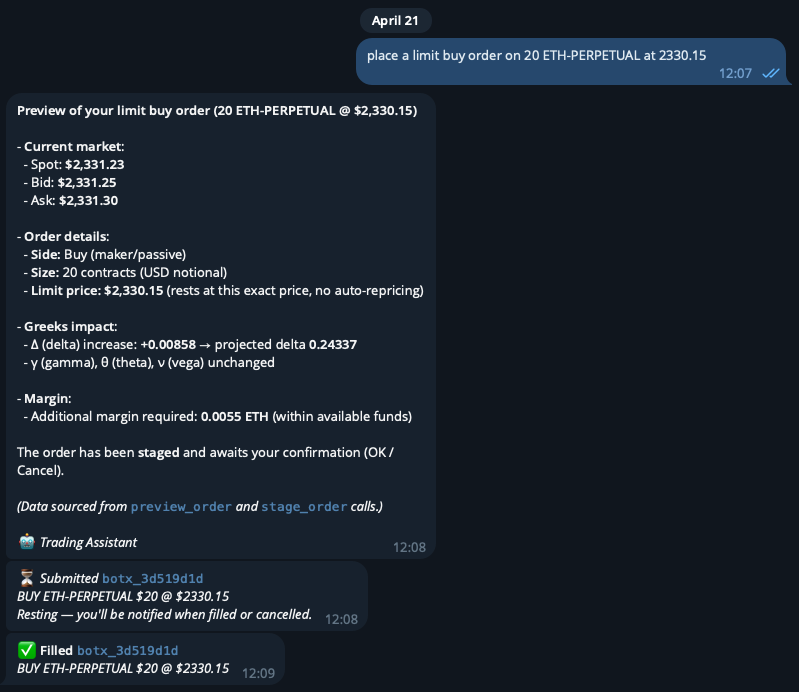

executorx — Order Execution

Manages order lifecycle end-to-end. Supports automated delta

hedging via perpetual rebalancing, implied

volatility-targeted limit orders, microstructure-driven

strategies using order book imbalance signals, and manual

order submission via the operator interface.

Rust / Svelte

dashboardx — Operations Dashboard

A real-time web dashboard streaming live position data,

Greeks, vol surface parameters, and order book state via

WebSocket. Provides a single-screen view of system health

and market exposure for the operations team.

Python / Go

botx + mcpx — LLM Interface

A PydanticAI-powered Telegram agent with access to the full

system via an MCP server (QuestDB, Redis, order submission).

Runs four concurrent scheduled loops: hourly volatility

reports, economic calendar digest, live signal forwarding

from strategyx, and hourly market data ingestion into

QuestDB.

Python / FastAPI

calibratorx — ML Model Host

Hosts a self-supervised ML models. Serves inference via REST

at runtime. Trained offline using walk-forward

cross-validation with Sharpe loss.

Rust

strategyx — Signal Runner

Evaluates ML strategy at regular time intervals. On each new

bar constructs the feature window, calls calibratorx for

inference, and — when signal strength exceeds threshold —

publishes a trade signal (direction, entry, take-profit,

stop-loss) to the Redis signal stream.